Chatbots in Banking: The Benefits of Using AI Automation

Chatbots in Banking: The Benefits of Using AI Automation

Customers of any type of business expect help instantly and access to their services in a growing number of ways. Banks are turning to chatbots to help deal with massive volumes of customer interactions. Conversational banking frees up agents for more complex issues, while the move to app-based and web banking sees customers more used to dealing with digital interfaces, of which chatbots and AI virtual assistants are just the latest step.

Established banks and their challenger rivals are all keen to develop a conversational banking strategy. Those that have been experimenting for some years find themselves with key advantages over banks stepping fresh into the conversational customer service arena.

Across Hong Kong, China, Europe and the Americas as the market hots up for connected banking services, much of the focus is on customer service efficiency, while some will have eyes on a future where blockchain and cryptocurrency or other services could play a part of people’s banking lives, and where bots will be faster and more useful than people in making transactions and offering advice.

The changing landscape for banking bots

For now, most banks want to reduce costs. Their consumer bank arms remain constrained either by customer desire for free banking in some countries or low-monthly fees in others. Bots help save on costly customer service centers either in-house or outsourced, and can answer the majority of customer questions without the need for an agent to get involved.

Beyond efficiencies, banks can also keep their more valued agents, with the promise of having a greater impact on the customer experience, handling queries that are too complex or personal for bots to handle, even as they become smarter through AI, natural language processing and training experience. For now, most bots handle balance checks, paying bills, transfers to linked accounts, making appointments and querying transactions.

Beyond the current state of affairs, banks will also need bots that can handle more complex transactions, such as Bitcoin and other cryptocurrencies. These are complex and require the use of third-party wallets and non-traditional destinations. Bots will be better able to handle the load and the complex back-end work, and other potential use cases for chatbots in banking

as cryptocurrencies become a normalised part of the business or personal finance market.

Bots will also be better able to offer advice on currency or crypto moves than a person, who would struggle to keep pace with such a fast-moving market. That’s as banks need to be smarter, offering a wider number of ways for customers to save money and to use their money more efficiently.

How the Banking Bots Work

Most bots are accessible from within the bank’s website portal or increasingly a mobile app to maintain security. Social media bots on Facebook Messenger can handle prospective customer or non-account queries, such as opening hours. While some banks use PIN codes to let people carry out secure tasks via Messenger.

But, for now, until authentication and ID assurance can cross devices and social media boundaries (think logging into a Facebook Messenger chat with your TouchID, FaceID, FaceTec or similar) the majority will remain behind the bank’s log-in services.

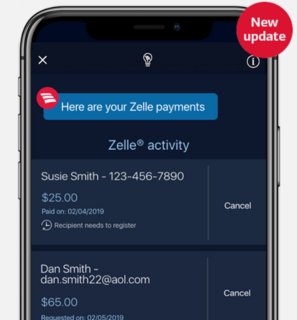

Most banks claim that their bots are AI enabled, but few have development stories about how they were built or their chatbot architecture, so it is hard to judge how smart they are. For now, few interact with other apps or services, but that will change. Bank of America’s app-based chatbot Erica is one of the few majors that does, interacting with Zelle, a third-party service for sending money to friends.

As customers get used to dealing with their bot the majority will find it saves them time on navigating a browser or app screens, and as bots get smarter they should offer a more personalised experience. This should increase customer loyalty, and make it easier for feedback on customer service beyond the usual “please take the quick survey after the call” or those “how did we do?” text message streams.

A well-designed chatbot will also be able to offer highly personalised marketing and offers that make sense to the customer in light of their usage and finances. And, as AI and machine learning experience grows, we will see innovation helping banks stand out from each other from making credit offers to help tailor investment plans.

As with most industries, AI automation enables 24/7 always-on support, efficiency savings for customer service automation. But, the AI aspect will lead to bots that can teach themselves new tricks, that can interact with other services to offer more information, and create new revenue opportunities for banks.

Across the banking market, new initiatives such as Open Banking and other FinTech trends allow the banks to unbundle and revalue services. Open Banking allows traditional and new banks to enable consent management, account aggregation and full data categorization. Chatbots can take their part in the process to explain the processes and help move their money to better products or money-saving and other initiatives.

The Best in Banking Chatbots

For more details on the current state of banking chatbot, check out these live examples of chatbots in the banking industry. Feel free to comment if you’ve had experience of a banking chatbot :

The most talked about chatbot in banking circles is Bank of America’s Erica. With over 6 million served since launch in 2017, she helps with transfers, balance checks and the usual range of consumer banking services to save customers time. However, BoA isn’t stopping there, with regular updates including financial insights for personalized and proactive guidance to help customers stay on top of their finances.

In Australia, the Commonwealth Bank uses a chatbot called Ceba to provide support for over 200 banking tasks - highlighting why banking bots need to be flexible and to address a wide range of needs. Tasks it can be asked vary from card activation to making payments. One key issue here is how any bank handles customer feedback. While it might be useful for most, Ceba comes in for lots of social media criticism, but the bank’s human agents are always on hand to reply and offer support or a solution.

Brazil’s Banco Itaú takes a very social approach to its Facebook Messenger chatbot, Alaor. It acts as financial advisor and savings guru to customers. offering tips on how the consumer can save or raise money and invest it appropriately. Also with a Latin flavour, Santander with operations in Europe and South America, has Sandrine to help customers resolver over 1,200 queries.

Up and coming banks around the world from North Africa to Asia are often leading the way and outstripping their western rivals in exposing customers to bots. In Lebanon, BOB helps Bank of Beruit customers choose from loans or accounts, and also talk to agents, not forgetting the human aspect of banking. United Bank for Africa’s Leo offers money transfers, payments and can help new accounts. Using Facebook Messenger, customers must use a PIN code to access account services.

In China, HSBC launched chatbot “Xiaofeng” and “Xiaohui” in 2018 for consumer and business banking customer queries, FX market updates. The company also launched a WeChat service account adding features like Payment Tracker and Trade Tracker for the popular Chinese social media service.

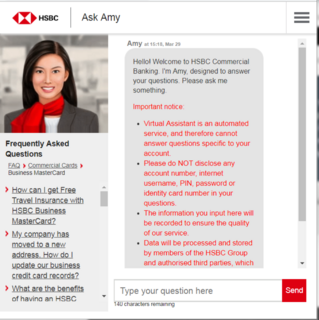

Breaking away from the consumer banks. Deutsche Bank has Debbie, helping finance traders work across markets to perform trades and so on. In Hong Kong, HSBC (again) has Amy, a friendly face for commercial bank customers. She doesn’t offer standard consumer banking queries, but can help with many of the wider aspects of business banking, from setting up accounts for different types of business, from sole traders to Limited Companies and other types. While these bots are far from the consumer world, they will help the businesses responsible learn more about the scope and limits of bots, and how they can impact everyone’s banking experience in the future.

and most Chinese and Indian banks lead their offerings with bots to deal with millions of requests.

Beyond the big name banks, challenger banks are using bots to augment their limited customer service, to partner with other providers or are looking at going all-digital on their support efforts. The likes of the UK’s Monzo has been using chatbot Plum to help customers analyse their spending or choose to invest in various savings tailored around themes such as ethical investments.

Where Banks Go Wrong (and can go Right) With Chatbots

Across all these banks and many more, there are varying levels of bot quality and service offering. Many banks still don’t have a chatbot, such as HBOS/Halifax in the UK. This demonstrates an industry that is both in flux and uncertain of how to proceed. Those that do chatbots well are clearly in a better position than those lagging behind.

Some banks just don’t seem to “get” technology. With feature limited or simple duplication of existing features. Take Lloyd’s Bank, one of the biggest names in the industry who’s chatbot, if you can call it that, is simply a replication of the company’s FAQ, with no effort at language understanding. Few, if any customers would find value from this,

Banks that have had poor early bot experiences might be concerned about future efforts, or at least launching without making a serious commitment to technology and development. But time is not on their side, as a generation of tech users grows up used to bots as part of their technology diet on mobile apps or social media.

Consumers want a fast and safe experience, that guarantees their security and privacy. The banks need to ensure their bot never pretends it is anything other than a machine. All its options need to be clear to the user, with issues like data retention and security explained on request.

New AI trends like deep learning, deep reinforcement learning, and automated machine learning will help make the bots better and more useful. Improvements in translation will make banks more accessible to a global audience, and banks can focus their bots on key areas like customer acquisition and brand management, moving beyond traditional customer service and account management. And that’s before banks need to start dealing with cryptocurrencies or blockchain transactions.

The Future for Banks and Bots

Disruption and transformation are common boardroom buzzwords for banks. People might soon switch banks as regular as they do phone or power provider. The chatbot will be a key tool in engaging and retaining customers, helping to build relationships, making them of interest to all but the most traditional of customers.

Banks large and small are all technology-focused, but their adoption of bots has been typical of other industries with successful market leaders and a host of failures. But bot builders and banks are learning fast what their customers needs and the bots of the 2020s will soon be a daily part of everyone’s lives, as they take over from traditional support avenues.

Whatever your bank’s current status, expect a bot to pay a more important part in the banking process in future, providing support and proactive advice to help us all save money. In an era of mobile-focused banking, digital wallets, cash sharing services and so on, all will need a bot as part of their service, but the banks will look to partner and build ecosystems to help keep the number of bots people deal with manageable.